In this post we look at the backtest results of selling a one-lot, at-the-money (ATM) straddle on the

S&P 500 Index (SPX), initiated at 38 days-to-expiration (DTE). In this second post of five on 38 DTE straddles, we look at trades that use the same loss exits as shown in the first post, and in addition, take profits at 10% of the credit received. The results displayed in this post represent data from more than 800 individual trades entered by the backtester.

For background on the setup for the backtests, as well as the nomenclature used in the charts and tables below, please see the introductory article for this series:

Option Straddle Series - P&L Exits.

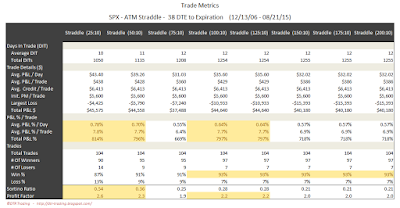

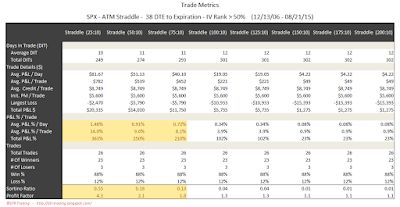

In the trade metrics tables, I've highlighted some of the metrics rows to indicate values that are in the upper half of the readings. One of the metrics to note is the average P&L per day in percentage terms (

P&L % / Trade - Avg. P&L / Day). This is a measure of the P&L per day normalized to the maximum

initial portfolio margin (initial PM) required for that trade run...it tells us the effectiveness of theta with respect to our margin requirement. Also note that the y-axis scale is the same in all of the 38 DTE equity curves.

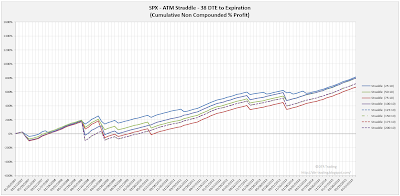

No IV Rank FilterIn this section we will look at the results of entering one trade for every monthly expiration regardless of the implied volatility (IV) rank of the SPX on the date of entry. Entering these trades at 38 DTE and utilizing our loss exits and 10% credit exits (described

here), resulted in the equity curves below.

|

| (click to enlarge) |

The trade metrics for these different exits are shown in the table below. The (25:10) variation stands out with the highest P&L % / day reading, highest overall P&L %, and a decent win rate...although not the highest in the group.

|

| (click to enlarge) |

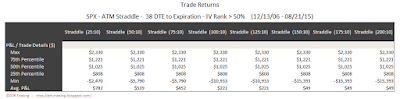

The table below shows the distribution of returns in

five-number summary format. Hat-tip to

tastytrade.

|

| (click to enlarge) |

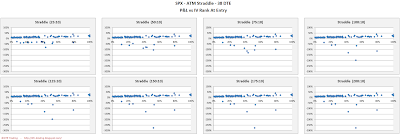

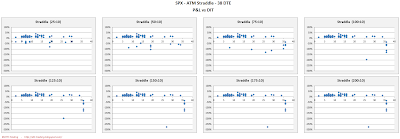

Below are three sets of scatter plots for selling 38 DTE ATM SPX straddles. The first image contains one scatter plot per strategy and shows P&L in percentage terms versus IV rank for the SPX. The IV rank was captured on the day each trade was initiated. There is a clear trend of increasing P&L with increasing IV rank.

|

| (click to enlarge) |

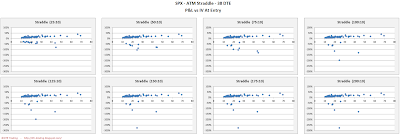

The next image shows P&L in percentage terms versus initial ATM IV. This ATM IV was captured on the day each trade was initiated. Higher IV resulted in higher returns, but the majority of the profitable trades occurred at lower IV.

|

| (click to enlarge) |

The third image shows P&L in percentage terms versus days-in-trade (DIT). When managing losses early (25%, 50%), the losses were fairly evenly distributed across DIT. As the loss management becomes less aggressive, we see that the losses are concentrated above 25 DIT...interesting!

|

| (click to enlarge) |

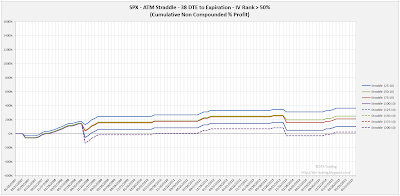

IV Rank > 50% FilterIn this section we will look at the results of entering one trade for every monthly expiration only when the IV rank of the SPX is

greater than 50% ( >50% ). Entering these trades at 38 DTE and utilizing our loss exits and 10% credit exits (described

here) resulted in the equity curves below.

|

| (click to enlarge) |

The trade metrics for these different exits are shown in the table below. There are significantly fewer trades that meet the >50% IVR criteria, but the P&L% per day readings are much higher at the lower loss levels (25%, 50%)

|

| (click to enlarge) |

The table below shows the distribution of returns in

five-number summary format.

|

| (click to enlarge) |

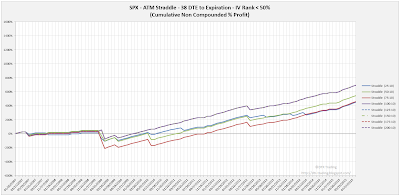

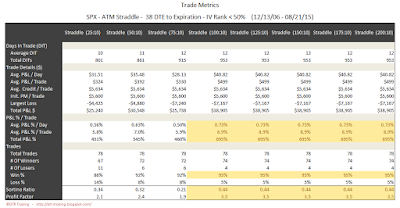

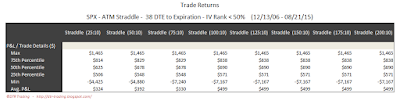

IV Rank < 50% FilterIn this section we will look at the results of entering one trade for every monthly expiration only when the IV rank of the SPX is

less than 50% ( <50% ). Entering these trades at 38 DTE and utilizing our loss exits and 10% credit exits (described

here) resulted in the equity curves below.

|

| (click to enlarge) |

The trade metrics for these different exits are shown in the table below. Using the lower IVR filter increased our win rate for the trades utilizing the larger loss exits, resulted in larger profit factor readings, and solid total P&L numbers....very interesting!

|

| (click to enlarge) |

The table below shows the distribution of returns in

five-number summary format.

|

| (click to enlarge) |

In the next post we will look at the backtest results of 38 DTE ATM SPX short straddles using the same loss thresholds as above, but with profit taking occurring at 25% of the credit received.

You can follow my blog by email, RSS or Twitter. All options are free, and are available on the top of the right hand navigation column under the headings "Subscribe To RSS Feed", "Follow By Email", and "Twitter". I follow blogs by RSS using Feedly, but any RSS reader will work.